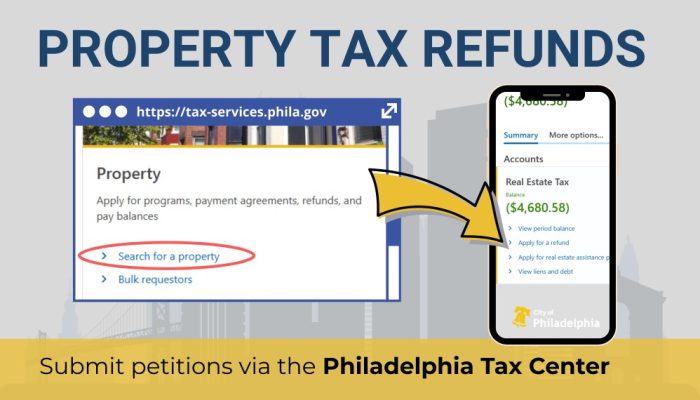

REDUCE YOUR PROPERTY TAXES: Use the combined application to apply for Homestead, LOOP, Installment Plans, and the Tax Freezes. Visit the Philadelphia Tax Center to get started! Read this blog post to learn more.

What we do

The Department of Revenue is committed to the accurate and timely collection of revenue to support City services and the School District of Philadelphia, while also striving to enroll all eligible customers in available assistance and relief programs. The Department is committed to providing customers with services they can see, touch, and feel by being accessible, transparent, and responsive.

Connect

| Address |

Municipal Services Building

1401 John F. Kennedy Blvd. Philadelphia, PA 19102 |

|---|---|

|

revenue |

|

| Phone |

(215) 685-6300

for water bills

(215) 686-9200

for LOOP and Homestead

|

| Social |

Get email updates

Stay up to date on all the latest tax regulations and Philadelphia Tax Center updates, including our self-service options!